Evolving climate accountability

A global review of public sector environmental reporting

Introduction

The climate crisis now sits at the top of global, political and economic agendas. Political priorities and economic imperatives have shifted abruptly in the past two decades, as the effects of climate change have become more evident.

The private sector has come under pressure from investors and consumers to recognise and mitigate its environmental impact. As a result, private sector companies are increasingly adopting non-financial reporting measures to better assess their performance and impact on the climate.

The practice of sustainability reporting, which draws together not only environmental but also social and economic measures, is now widespread in the private sector. This is an incredibly positive trend. Knowing and understanding the impact of your actions is essential if we are to effectively mitigate climate change and make our societies more sustainable.

But sustainability reporting in the public sector is in a markedly different place. Public sector organisations are lagging behind their private sector counterparts.

CIPFA set out to identify what, if anything, public sector organisations around the world are doing to report their impact on the climate. We surveyed public sector professionals around the world and hosted a series of regional roundtables. Participants included public sector accountants, practitioners, academics, auditors, public servants and standard-setters.

Although knowledge gaps surely exist, this research is intended to provide a baseline from which the evolution of public sector sustainability reporting can be measured.

Public sector context

The public sector is the largest economic sector of most nations. As such, it has an enormous impact on not only the economy, but also society and the environment. The public sector has a dual role: as a provider of public services – like the armed forces, law enforcement, public healthcare systems, emergency services and education – and as a regulator, setting rules and standards for business, society and itself. This means the public sector impacts the environment and climate both directly via its own activities and indirectly through the regulation of wider players in its economy.

Carbon is carbon – the planet doesn’t care who produced it.

Public sector objectives are fundamentally linked to public interest and benefit. With that in mind, public sector organisations have strong incentives to report on and account for their impact on the environment, social wellbeing and prosperity.

Taxpayers and citizens also have a vested interest in how public sector bodies are addressing sustainability challenges. Public interest in climate change is growing and sustainability reporting enables governments to demonstrate how they are addressing the most pressing challenge of our generation. It also holds them accountable for their environmental performance.

The challenge for public sector sustainability reporting is multi-faceted:

- It can have many definitions, which can influence the scope and focus of the report.

- There are a multitude of standards for sustainability reporting, but few refer directly to the public sector context.

- Differences between private and public organisations (their purpose, motivation and responsibilities) impact the way sustainability reporting is conducted.

The findings

What we found: the current landscape

Sustainability reporting is in its infancy in the public sector. Less than half of those who responded to our survey were currently preparing sustainability reports.

However, there is clearly a desire for such reporting. There is a consistent view that public sector organisations should not delay their sustainability reporting journey, as the process will need to evolve and adapt over time.

Parameters for reporting

At present, there is no clear and agreed definition for this type of reporting in the public sector. Among those preparing such reports, there is no standard interpretation of what constitutes climate-related, or environmental, reporting.

Confusion is our enemy.

We identified 12 sustainability reporting frameworks that could potentially be used to report on climate matters.

However, none of these deal specifically with the public sector.

Among those who are preparing sustainability reports, there is no consistency in the framework they chose to use. There is strong agreement that work to align and harmonise existing frameworks should be a priority and that consideration should be given to their application in the public sector.

Committing to sustainability reporting

Sustainability information is often reported on a voluntary basis in public sector organisations. Very few international jurisdictions have made sustainability reporting mandatory for public sector organisations.

The absence of a mandate for this type of reporting has prevented it from becoming mainstream in the public sector. However, it was recognised that this needs careful consideration:

Mandating this type of reporting for the public sector is a complicated issue. Before it can be done, there must be an analysis of what is already mandated in that jurisdiction and what reporting is already done to avoid duplication of effort.

Institutional commitment is viewed as an essential prerequisite for sustainability reporting to materialise as common practice in the public sector.

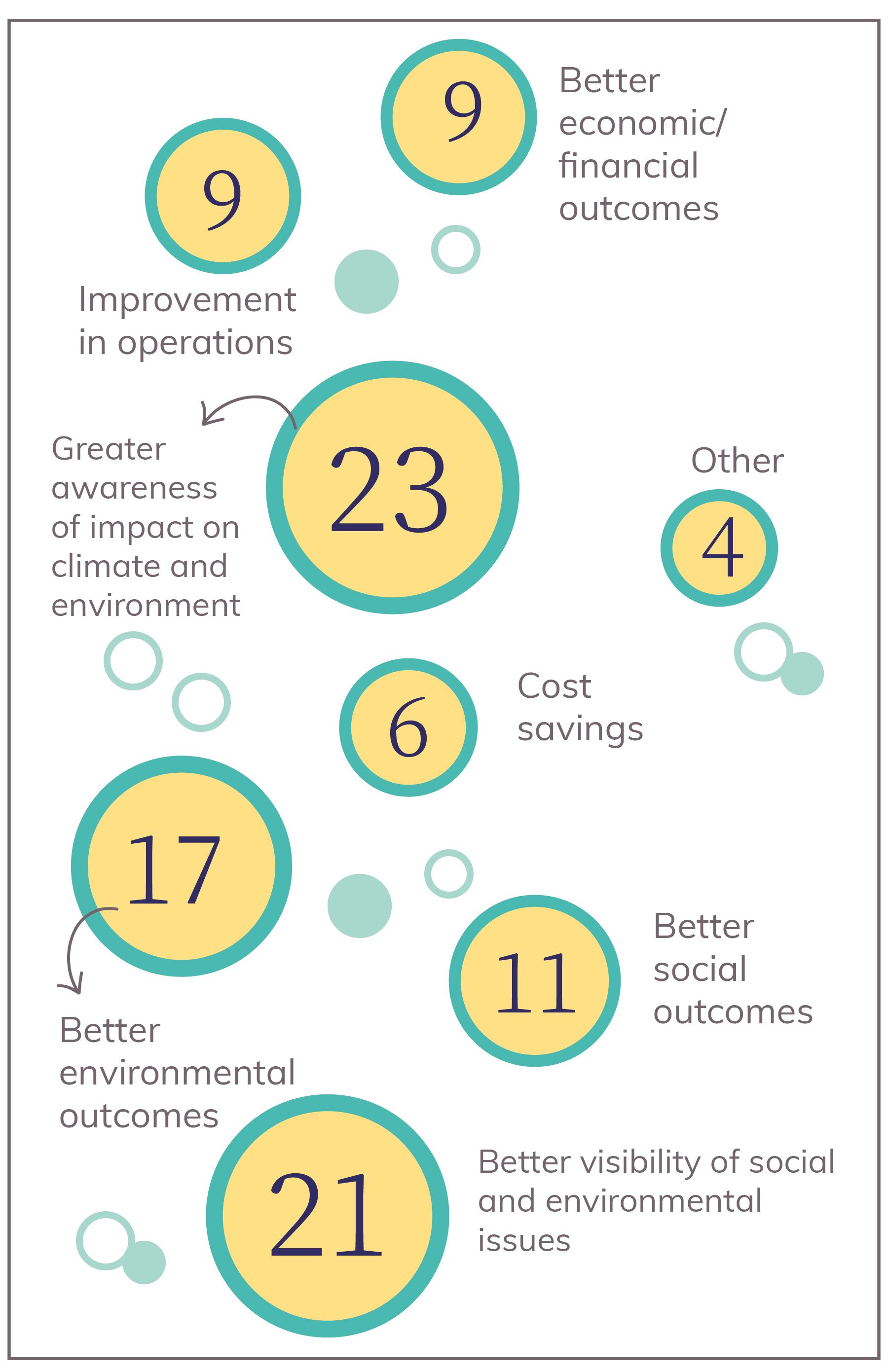

Benefits of reporting

For those producing a sustainability report, a number of benefits were identified, the most common being greater awareness of the impact of the organisation on the climate and natural environment.

Benefits of sustainability reporting according to respondents (%)

This suggests that once a sustainability report is being prepared, the information is valuable in influencing decisions and delivering better outcomes on environmental and social matters.

What we found: preparing sustainability reports

Less than half of the people we surveyed (44%) confirmed that their organisation prepares a sustainability report. Among those that have prepared a sustainability report, only two thirds (66%) used an established framework to do so.

The absence of the following are the key limitations for preparing sustainability reports:

- Quality data.

- A public sector framework.

- Mandates to produce a sustainability report.

Harmonisation across frameworks is viewed as a priority, with a particular focus on the public sector context.

Purpose and audience

There is broad public interest in the activity and impact of government activity and the public sector. The majority of those producing a sustainability report identified the general public/community as their primary reason for producing a report.

Main purpose for preparing a sustainability report (%)

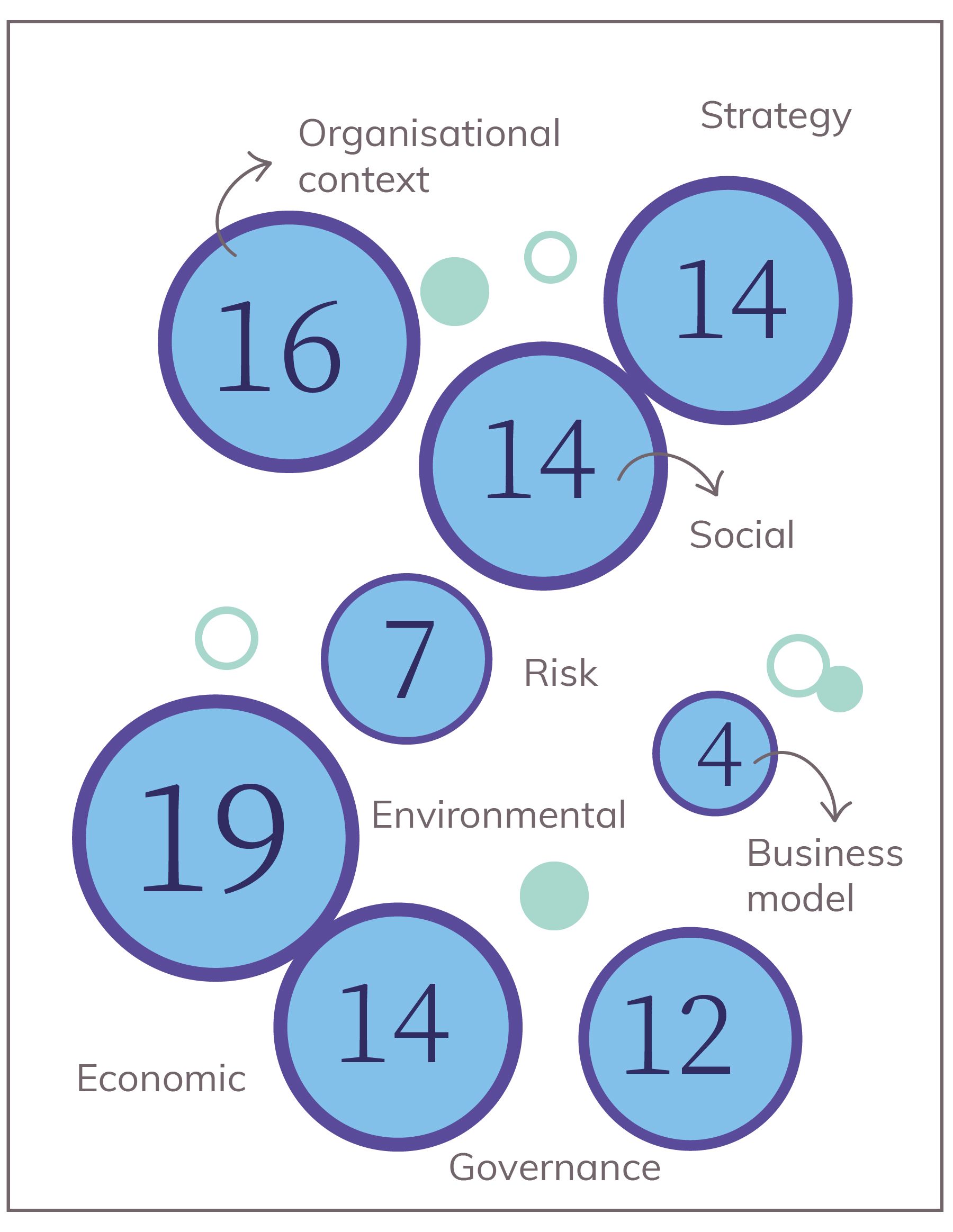

Content of reports

Although there was little consistency in the approach being taken to sustainability reporting, the content included in reports is similar.

Commonly included sections in public sector sustainability reports (%)

Challenges involved

We identified a number of obstacles to producing sustainability reports. The lack of quality data was the most commonly cited issue, followed by a lack of accepted framework and political support.

Challenges to preparing a sustainability report (%)

Policy alignment

The research suggests that the take-up of sustainability reporting in the public sector has also been limited by the absence of a clear policy. We found that among professionals who stated that their organisation’s policy work supported sustainability reporting, all had prepared a sustainability report.

Additionally, almost 60% of those reporting on sustainability included targets for the measures identified in their report, the majority of which were done on an annual basis. Interestingly, few identified how these targets were approved.

Type of target (%)

What we found: assurance and accountability

Assurance is viewed as essential for ensuring sustainability reports are reliable and credible. Assurance also mitigates the potential risk of ‘greenwashing’ However, only 25% of reports prepared were subject to an audit or verification process.

If sustainability reporting is not mandatory and not audited, it’s really not worthwhile.

Two main challenges in auditing sustainability reports were identified:

- The absence of an established framework for preparing reports.

- The absence of specific auditing standards or guidance.

Challenges in auditing sustainability reports (%)

Auditors remain concerned that unfavourable audit outcomes early on could limit further uptake of sustainability reporting in the public sector. With no reporting mandate in place, a phased approach to auditing and assuring sustainability reports may be worthwhile until the exercise matures.

At present, sustainability report audits are generally conducted by an external third party, supported by internal resources rather than the relevant supreme audit institution (SAI). The lack of SAI involvement in the audit and verification process is seen as a limit for accountability arrangements in the sector.

SAIs are really good at getting parliaments and their committees involved in any issues that they audit.

Accountability mechanisms applied to sustainability reports also appear to be limited, with only 17% stating that their reports are subject to scrutiny. However, some jurisdictions have already implemented institutional arrangements linked to climate concerns – such as dedicated parliamentary committees – which can add momentum and demand for this type of information.

What we found: capacity, capability and communication

The capacity and capability of staff were recognised as essential to the preparation of sustainability reports. The lack of specialised climate science expertise among staff was highlighted as a particular issue, with 60% of those currently reporting having a dedicated sustainability area responsible for the preparation of the report.

Only 37% of those preparing a report believed that they had sufficient skills...

...and only 34% believed that they had sufficient staffing capacity to meet the requirements of sustainability reporting in the future.

Having the necessary climate expertise affects not just the preparation of a report, but also the audit and/or verification of a report – there are knowledge gaps on both sides of the accounting equation. Broader skills and expertise are required for sustainability reporting practice to become mainstream.

There was also recognition that although much environmental information is non-financial in nature, the finance profession can play a leading role, particularly in the establishment of controls and systems for the collection and reporting of data to be included in sustainability reports.

In practice, the integration of sustainability information into wider reporting was fairly limited. While the release of standalone information can assist in raising awareness and increase the focus on sustainability information, integration with other forms of reporting is critical. Integration provides a more comprehensive picture of the entity’s overall performance and can better inform decision making.

Are reports integrated? (%)

Communicating sustainability information in the public sector is still not as effective as it could be. The majority of research participants preparing reports stated they only use one channel to communicate their report.

Future considerations

We identified seven areas for consideration in order for sustainability reporting to become a mainstream part of public sector external reporting.

1. Clarity on the definition and scope of sustainability reports to ensure a common understanding and interpretation of what constitutes public sector sustainability reporting.

2. Accelerating the alignment and harmonisation of existing frameworks and standards, with a view to adopting a framework that is appropriate for the public sector to underpin sustainability reporting.

3. Committing to public sector sustainability reporting at an institutional and organisational level to add impetus to the maturation and evolution of reporting.

4. Prioritising the development of the broader skill set and expertise needed to support high-quality sustainability reporting and any related audit or assurance activities.

5. Recognition of the key role of assurance in sustainability reporting and the consideration of ‘phasing in’ assurance arrangements, given the relatively immature nature of reporting in the public sector.

6. Integration with wider forms of reporting to avoid duplication, provide a holistic view of organisational performance and better inform decision making.

7. Promoting and strengthening institutional arrangements for the oversight and scrutiny of sustainability reports.

The public sector is trailing the corporate sector on sustainability reporting. However, there is a strong appetite for this type of reporting in the public sector around the world. The professional consensus is that governments and public entities should not delay, but rather begin reporting their climate impact as soon as possible, even if the first reports are rudimentary. The focus should now be on removing the key barriers that exist across the global public sector to make sustainability reporting as straightforward and achievable as possible.

Our climate is changing, and time is not on our side. A pan-public sector effort is urgently needed to accelerate the adoption and adaptation of this form of reporting.

Copyright ©2021 CIPFA

CIPFA, registered with the Charity Commissioners of England and Wales No. 231060 and the Office of the Scottish Charity Regulator No. SC037963.

CIPFA Business Limited, the trading arm of CIPFA that provides a range of services to public sector clients, registered in England and Wales no. 2376684.

Registered Office 77 Mansell Street, London E1 8AN